Banks Cook Books to Promote Wrong Choice Act, Attack CFPB

By Ed Mierzwinski, U.S. PIRG

Today the House Financial Services Committee is considering (marking-up or voting on) the so-called Financial Choice Act, which we call a Wrong Choice or a Cruel Choice, to repeal the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 and leave the CFPB an unrecognizable husk incapable of protecting consumers. Our main PIRG opposition letter is here. Numerous other letters of opposition from consumer, civil rights, labor and investor protection groups are archived here.

But I’ve detailed our opposition before. Today, I simply want to expose the false narrative that some 52 state bank associations are using in support of the bill, based on a “cook-the-history-books” analysis of bank consolidation. Their claims are based on preposterous abuse of math, simple math.

In the first paragraph of a letter to the committee, the associations claim:

Since the enactment of the Dodd-Frank Act, 1,917 banks—24% of the industry—have merged or closed their doors. Today, there are less than 6,000 banks in this country for the first time since 1890. While economic conditions and other factors certainly play a role in any bank’s closure or merger, it would be shortsighted to believe that the influx of new regulations over the past decade have not contributed to this rapid decline in the number of banks serving their communities. In fact, the pace of consolidation jumped dramatically after the enactment of Dodd-Frank, from a decline of 14% six years before the law was enacted, compared with a decline of 24% after it.

Their data set is incomplete and intended to deceive. Six years before the passage of Dodd-Frank was July 2004. That was during the peak of the mortgage bubble. Banks weren’t closing; they were growing, rising on a dangerous, frothy, toxic unregulated mix of reckless practices.

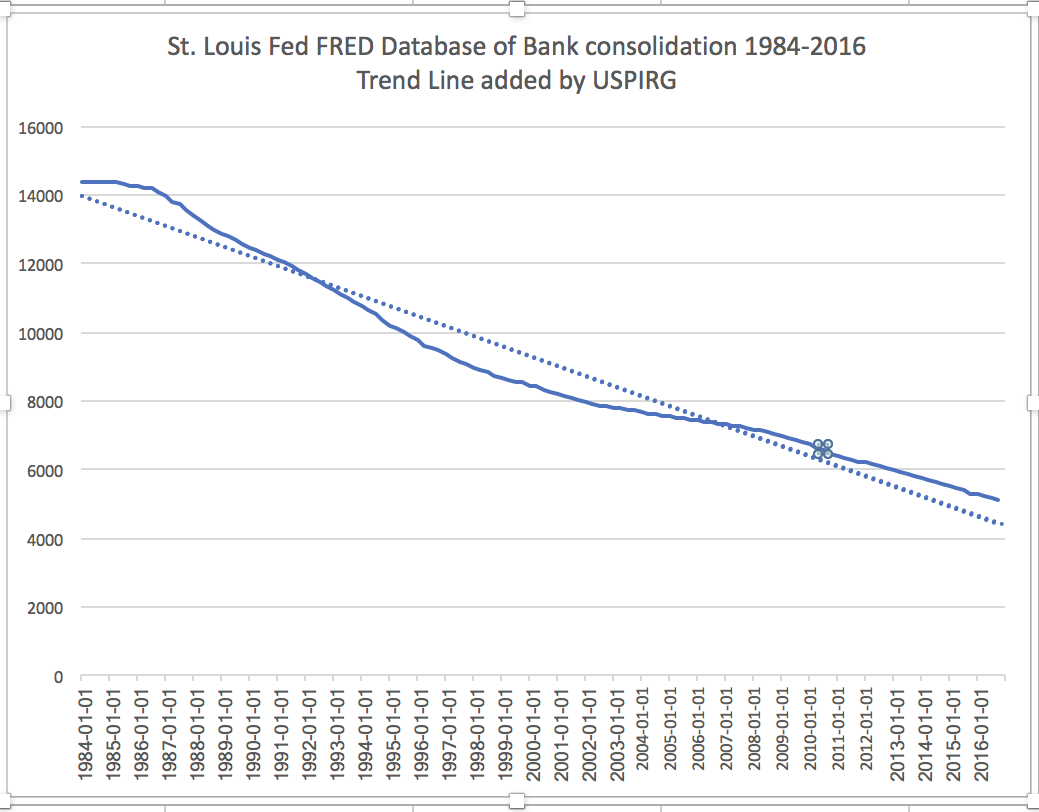

Blaming the consolidation of the bank sector on passage of the Dodd-Frank Act cannot be shown by the available data. I took a look at the authoritative FRED “Commercial banks in the U.S.” data set of the Federal Reserve Bank of St. Louis. You can see steady consolidation (including mergers, not only failures) since 1984; not merely since the Dodd-Frank Act’s passage. From over 14,000 banks in 1984, there has been a nearly steady consolidation, an overall change of -64%.

Blaming the consolidation of the bank sector on passage of the Dodd-Frank Act cannot be shown by the available data. I took a look at the authoritative FRED “Commercial banks in the U.S.” data set of the Federal Reserve Bank of St. Louis. You can see steady consolidation (including mergers, not only failures) since 1984; not merely since the Dodd-Frank Act’s passage. From over 14,000 banks in 1984, there has been a nearly steady consolidation, an overall change of -64%.

The trend line I added shows that, in fact, since 2010 (the asterisk), actual consolidation is at a lesser rate than the overall 1984-2016 trend shows. If you go to the actual FRED page, it also adds shading showing periods of recession.

The Center for American Progress has done much more detailed work on false Dodd-Frank narratives and the trend of bank consolidation here and here and here. As Sarah Edelman explains in the second link:

Why are there fewer community banks now than there were in the 1980s? Over the past 30 years, more than 80 percent of the banks that have exited the market have not failed. Rather, they have merged with unaffiliated banks or consolidated with other chartered banks, sometimes within the same organization. Larger banks can benefit from the economies of scale that make certain operations more efficient. Community banks also have fallen victim to the population loss and economic challenges afflicting rural communities; 86 percent of rural counties in the Great Plains states, for example, experienced population loss between 1980 and 2010. Unlike larger banks, which may have branches across states and geographic areas, community banks are especially vulnerable to declines in their local customer base.

Sarah goes on to further explain that, despite their false claims of economic pain, small banks are doing well, as are all banks. Don’t believe the non-profit CAP? Then check out the latest from the FDIC, which also explains banks are doing well.

I would also point out that Chairman Hensarling routinely claims that community banks will be the main beneficiaries of the Financial Choice Act. In fact, its provisions designed to help smaller institutions are, at best, a teeny caboose on a massive Wall Street train. The Financial Choice Act is the wrong choice for consumers, depositors, small investors, taxpayers and the economy itself.

In particular, the CFPB has been a huge success, restoring fair rules of the road to a financial system that let banks run amok, leaving millions without homes, millions more without jobs and millions more with trillions in lost retirement income. The idea of the CFPB needs no defense, only more defenders.